July 17, 2017

Have

Bundesbank Agents Infiltrated the Fed?

Germany’s central bank is the Bundesbank. Prior to the commencement of

trading of the euro in January 1999, the Bundesbank conducted Germany’s

monetary policy. The Bundesbank has a reputation for pursuing general

price-level stability above all else. You might say that the Bundesbank has

inflation phobia. The reason for this Bundesbank inflation phobia is the

remembrance of the hyperinflation Germany experienced between World Wars I and

II. Given the U.S. central bank’s recent actions, it would almost seem that the

Fed has developed inflation phobia too.

Although the U.S. does not have general price-level stability, the rate

of change of the consumer price index (CPI), no matter how you slice or dice

it, is absolutely low. This is illustrated in Chart 1. Plotted in Chart 1 are

the 12-month percentages changes in monthly observations of various CPI

measures – the CPI including all of its goods/services items, the CPI excluding

its energy goods/services items and the Cleveland Fed’s 16% trimmed-mean CPI.

The 16% trimmed-mean CPI eliminates components showing extreme monthly price

changes. Eight percent of the weighted components with the highest and lowest

one-month price changes are eliminated and the mean is calculated from the

remaining components, making the 16% trimmed- mean CPI less volatile than

either the CPI or the CPI excluding prices for energy goods/services. In the 12

months ended June 2017, the percentage changes in the CPI with all items, the

CPI excluding energy items and the 16% trimmed-mean CPI were 1.6%, 1.6% and

1.9%, respectively. Moreover, the 12-month percentage change in the CPI, no

matter how you measure it, has been trending lower since the first two months

of 2017.

Chart 1

Plotted in Chart 2 are the three-month annualized percentage changes in

the same variations of the CPI. In the three months ended June 2017, the

annualized percentage changes in the CPI with all items, the CPI excluding

energy items and the 16% trimmed-mean CPI were 0.06%, 1.05% and 1.05%,

respectively.

Chart 2

Admittedly, this does not represent literal general price-level

stability, but these rates of consumer price inflation are low in an historical

context and in absolute terms. Of course, just because price inflation

currently is quiescent does not mean that it will remain quiescent. According

to the late and great economist, Milton Friedman, inflation is always and

everywhere a monetary phenomenon. Has the Fed sown the monetary seeds of future

higher inflation? To answer this question, consider the data in Chart 3.

Plotted in Chart 3 are the year-over-year percent changes in the annual average

observations of the sum of depository institution credit and the monetary base

(currency plus reserves of depository institutions held at the Fed) along with

the year-over-year percent changes in the annual average observations of the

Personal Consumption Expenditures chain price index. As regular readers of my

irregular commentaries recall, the sum of depository institution credit and the

monetary base is what I call “thin-air” credit because both components are

created figuratively out of thin air. In Chart 3, observations of thin-air

credit growth have been advanced by

two years because this results in the highest correlation coefficient, 0.59,

between the two series. That is, from 1953 through 2016, the highest

correlation between growth in thin-air credit and consumer inflation occurs

when growth in thin-air credit leads

consumer inflation by two years. So, what is happening to thin-air credit

growth today has its maximum effect

on consumer inflation two years later.

(This has important implications as to how U.S. monetary policy should be

conducted, but the discussion of this is for a later commentary.) Thin-air credit grew 5.7% in 2013, 6.7% in

2014, 4.0% in 2015 and 4.3% in 2016. (As a point of reference, the median

year-over-year growth in thin-air credit from 1953 through 2016 was 7.1%.) So,

growth in thin-air credit slowed in 2015 and 2016 from its growth in 2013 and

2014, suggesting that consumer inflation should slow in 2017 and 2018 compared with 2015 and 2016.

Chart 3

Let’s home in on the recent monthly behavior of thin-air credit.

Plotted in Chart 4 are the 12-month percent changes in the sum of commercial

bank credit and the monetary base along with the end-of-month Federal Open

Market Committee (FOMC) target levels for the federal funds rate. Note that

growth in this subcomponent of thin-air credit has been trending lower in recent years, slowing to 2.6%

in the 12 months ended June 2017. Notice also that the federal funds rate has

been trending higher. Coincidence? I

don’t think so.

Chart 4

In order for the Fed to push the federal funds rate higher, it must

reduce the supply of the monetary base

relative to the demand for the

monetary base. Chart 5 shows that as the target level of the federal funds rate

was increased by one full percentage

point in the 19 months ended June 2017, the monetary base contracted by $308 billion.

Chart 5

As the federal funds rate moves higher, banks’ loan rates move higher,

too. As bank loan rates move higher, the quantity demanded of bank credit

decreases. Chart 6 shows that the 12-month growth rate in bank credit has been

decelerating as the federal funds rate has been rising, especially so starting

in late 2016.

Chart 6

To reiterate, not only is the current rate of consumer inflation low,

but the slowing in the growth of thin-air credit suggests that the rate of

inflation two years from now will remain low. While the lag between thin-air

credit growth and inflation is about two years, the lag between thin-air credit

growth and growth in real aggregate

demand for goods and services is much shorter. And for those who don’t have

their heads in the sand, the evidence of this abounds. Real GDP growth in the

1Q:2017 was a paltry 1.4% annualized. And although second-quarter real GDP

growth is likely to be higher than that of the first quarter, it is unlikely to

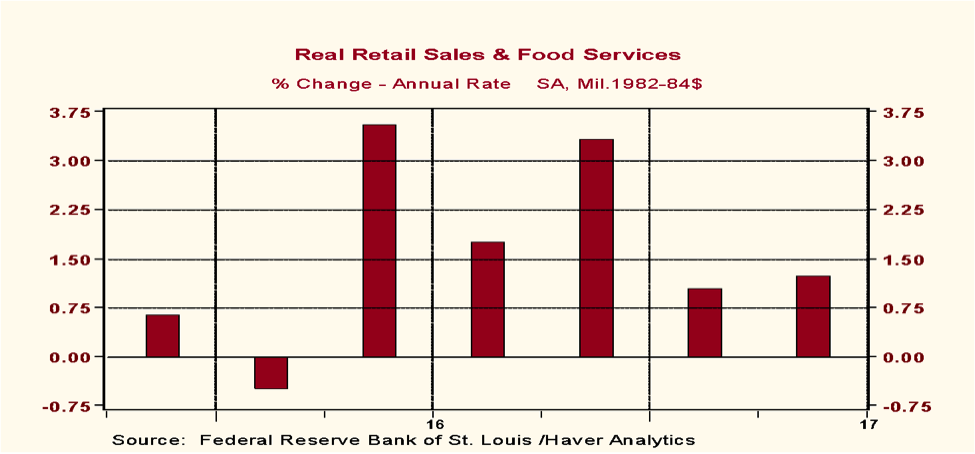

be that much higher. As shown in Chart 7, annualized growth in second-quarter

real retail sales was 1.3%, only marginally faster than the first quarter’s

1.1%. Nominal private construction spending contracted

at an annualized 4.7% in the two months ended May, as shown in Chart 8.

Shipments of manufactured goods have stalled out after their December 2016

surge (see Chart 9). Annualized growth in manufacturing production slowed to

1.4% in the second quarter vs. 2.1% in the first quarter (see Chart 10).

Chart 7

Chart 8

Chart 9

Chart 10

Allegedly, nonfarm payrolls increased by 581 thousand in the three

months ended June 2017. There must have been more frequent and longer coffee

breaks because the sales and production data do not point to much being

produced or sold. Perhaps employers are hiring in anticipation of the big

public/private infrastructure program talked about during the last presidential

campaign.

Fed officials indicate that there is at least one more hike in the

federal funds rate coming in 2017. Why would the Fed want to do this in the

face of low inflation and weak economic growth? Fed officials indicate that the

Fed will begin paring down its holdings of securities at some point in 2017.

All else the same, a decline in Fed securities holdings will reduce the

monetary base. All else the same, a reduction in the monetary base will result

in an increase in the federal funds rate. Why does the Fed feel the necessity

to reduce its holdings of securities in the face of low inflation and weak

economic growth?

Does the Fed have a working

monetary policy compass? The chairman of the House Financial Services

Committee, Representative Jeb Hensarling of Texas, is in favor of the Fed

determining and announcing some rule

to guide the FOMC on its monetary policy decisions. President Trump has

nominated Randal Quarles for one of the three vacant Fed Board governors’

seats. Although primary remit of Quarles will be regulatory supervision of

financial institutions, when (not if) confirmed by the Senate, he will have one

vote on the FOMC. According to a Politico article, Quarles is in favor of the Fed

using the Taylor Rule as the compass by which monetary

policy is navigated. Governor Yellen’s term as chairperson of the Federal

Reserve Board ends February 3, 2018. If she is not re-nominated by President

Trump, which I believe is a high probability outcome, she would likely resign

from the Federal Reserve Board rather than remain as a mere governor. What all

of this implies is that President Trump will likely have nominated and the

Senate confirmed four of the seven governorships to the Federal Reserve Board

by February 2018, one of whom will be the next chairperson. Who knows, one of

the nominees might even be John Taylor, the namesake of the Taylor Rule.

Regardless, there is going to be increasing pressure on the Fed to adopt some

rule to guide its monetary policy decisions, especially with real economic

growth disappointing in 2017. Perhaps in my next commentary I will discuss why

the Taylor Rule is the wrong rule for

the Fed to adopt. Can you guess what might be involved in the rule I would

favor?

This is the first commentary I have published

since early April. I appreciate those of you who have inquired as to my health

or whether I have run off to play the bass guitar in a blues band. My health

appears to be good. Not so my bass guitar playing. Some of my time was spent

putting together presentations for Legacy Private Trust Company, the contents

of which I have covered in my previous commentaries. Similar to President

Trump, I have been watching too much television. As an antidote to the news, I

got hooked on a Netflix comedy series, “Rake”. The series revolves

around a rakish (hence, its name) Aussie defense lawyer. In the first episode

of Season 1, the lawyer agrees to defend a prominent Australian economist who

is charged with murder. Did I mention that the economist is an admitted

cannibal? Talk about putting the “dismal” in the dismal science! I took some

time out to walk my lovely daughter down the aisle in her marriage to fine

young man (who knows his Seinfeld better than I). Lastly, I have been occupied

with a 50th anniversary gift from my wife, a beautifully restored

50-year old classic sailboat – a Pearson Commander 26. I will try to be more

productive, but sailing season up here in tundraland lasts until early October!

Paul L. Kasriel

Founder, Econtrarian,

LLC

Senior Economic and Investment Advisor

1-920-818-0236

“For most of human

history, it made good adaptive sense to be fearful and emphasize the negative;

any mistake could be fatal”, Joost Swarte

You're back! hallelujah.. I thought you may have passed to the great beyond. Lol

ReplyDelete'Can you guess what might be involved in the rule I would favor?'

ReplyDelete(a) a bass guitar (b) a sailboat (c) something with air

I agree the Fed is worried turned into Bundesbank-lite. They're not paying attention to the monetary aggregates. They're focused on the Taylor rule for now, as that is the only thing that allows them to justify tightening supply of money in anticipation of future (unlikely) inflation. There has been no substantial wage gains, CPI, PPI, or monetary base expansion, so almost everything else points against their current actions

ReplyDeleteeuh, you seem, like (the bass playing as opposed to the late 1990's) Dr. Kasriel, to ignore the massive asset inflation that has taken place (yes, it's a giant bubble) and several (other) negative consequences of the current low interest rate environment (e.g., lower productivity because of the survival of not so fit zombie companies, cf Japan)

DeleteTestimony of financial breakthrough from GOD through the help of Funding Circle Loan INC. (fundingcapitalplc@gmail.com OR Call/Text +14067326622)...

ReplyDeleteHi I'am Evelyn Russell resident at 808 NE 19th St Oklahoma City, I am a single mother blessed with 2 daughters. For a while now I have been searching for a genuine loan lender who could help me with a loan as I no longer have a job, all I got were hoodlums who made me trust them and at the end they took my money without giving me any loan, my hope was lost, I got confused and frustrated, it became difficult for my family to feed with a good meal, I never wanted to have anything to do with any loan lending companies on the internet again. Not until I met a Godsent loan lender that changed my life and that of my family Through the help of a fellowship member "a lender with the fear of God in him Mr JASON RAYMOND, he was the man God sent to elevate my family from suffering. At first I thought it wasn’t going to be possible due to my previous experience until I received my loan worth $135,000.00 USD in less then 24hours. So my advise to anyone out there genuinely in need of a loan is to contact Funding Circle Loan INC through this official email:- fundingcapitalplc@gmail.com OR Call/Text +14067326622 and be financial lifted.

BETTERMENT FUNDING {bettermentfunding@gmail.com}

ReplyDeleteHi everyone, i am Alexis Ohanian am so glade coming back to this great forum to testify about the help i received from Chester Brian. I was in desperate need of a loan in other to be free from debt and financial bondage that was place on me by my ex husband. It was really bad that i have to seek for help from Friends,family and even my bank but on one could assist me because my credit score was really bad. So i was browsing with my computer and saw some testimonies from people Chester Brian assisted with a loan, then i decided to contact him on his email {bettermentfunding@gmail.com}, then i received a mail from them and i did all that was asked from me. To my greatest surprise they transferred to my account the loan i requested and now i am so happy clearing my debt and have also started a business with the remaining amount to take care of myself and family. If you need a loan do contact the best loan lender of all time Chester Brian on his email: {bettermentfunding@gmail.com}

..